How Should Banks Invest in the Digital Experience?

Learn how to interpret customers’ online behavior to understand their preferences and better cater to their needs, even if you’re not physically with them.

A friendly hello from a banker who knows your name when you walk into the branch used to be the mark of a good customer experience.

Those personal moments in the analog age now have to be replicated in today’s digital, multi-channel world. With added restrictions from COVID, financial providers and banks are under increased pressure to personalize their digital offerings to deliver the “you know me” service that customers expect.

The Basics: Understand Customers’ Preferences

In a recent webinar, Chef sara bradley from Kentucky restaurant freight house shared how difficult it was to not have live feedback from a customer. Did they clean their plate? Are they happy after their meal? With to-go options only, it can be more difficult to understand a customer’s experience.

The same goes for digital-first experiences.

Businesses must prioritize interpreting customers’ online behavior to understand their preferences and better cater to their needs, even if they’re not physically with them.

Financial services organizations should capture signals such as what people click on, what types of accounts they research, the offers they ignore, the language they use to search, and when they reach out to customer support.

Through collecting and analyzing these signals, financial services organizations can turn customer actions into insights to predict customer intent and make proactive recommendations, sometimes before they’ve ever asked the business for assistance.

Investing in Digital Post-Covid

Even before we had to wear face masks and stand six feet apart while waiting in line, a survey from Adobe found that “nearly nine in ten consumers (89%) use their bank or credit union’s online banking option, and just over half of them (52%) conduct most of their banking online.”

The survey also reported that nearly 59% of consumers would not do business with a financial institution that didn’t offer digital or mobile banking services. This was particularly true of Millennial and Gen Z consumers.

It’s especially difficult to replicate valuable opportunities to consult with depositors and investors in-person.

Those consultations are an important part of the sales cycle for high-margin products. Organizations will need to accelerate their investment in digital customer touchpoint technologies in order to preserve those sales opportunities.

The Question Is, Where to Start?

There are three emerging trends: the shift towards cloud computing, the rise of question-answering systems, and the adoption of digital voice assistants.

Cost Savings With Cloud Computing

According to Lucidworks CEO Will Hayes: “Across the Global 2000, every enterprise conversation of late has been focused on cloud. It’s exciting to see the acceleration of this transition to the cloud happening before our eyes. A portion of the business we assumed would be on prem is now moving to the cloud.”

As the security of public cloud infrastructures reaches parity with on-premise data centers, more banks shift towards cloud computing.

This is a win-win because it reduces the cost of maintaining a diverse array of digital touchpoints, and allows resources to be redirected into improving the digital experience.

Make Chatbots and Virtual Assistants Smarter

Many question-answering systems are nothing more than keyword matches with a robust FAQ.

Advancements with NLP (natural language processing) make it possible to understand a wide array of sentence structures (even with misspellings) and retrieve the right answer so customers can ask questions online through a chatbot or search bar the same way they would speak with a customer service representative in person.

Financial service organizations that invest in question-answering systems can mimic natural language interactions between a customer and a member of staff. With advancements in deep learning, those conversational frameworks can learn for themselves and understand more subtle human nuance, which is useful in the absence of in-person interactions.

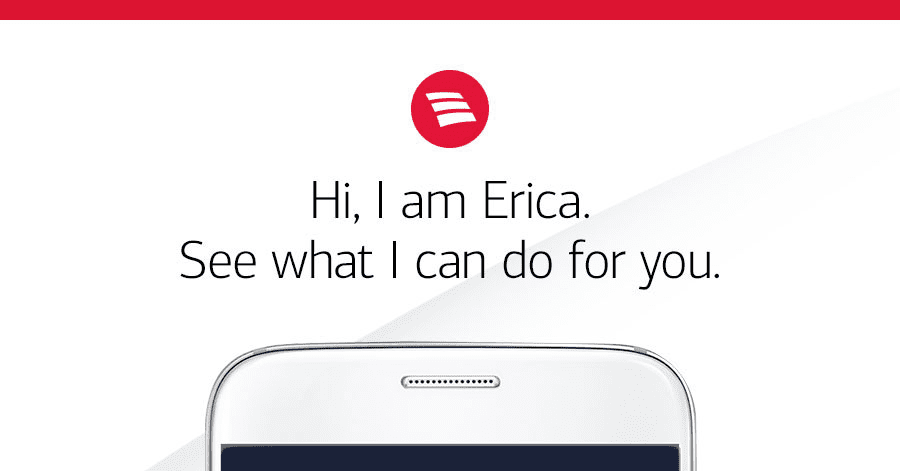

Free up Advisors With Voice Assistants

Bank of America, an early adopter in the industry, launched its voice activated assistant, Erica, in 2016. In March of 2019, it announced a suite of enhancements to the product, and reported that in under three years it had amassed more than six million users, answered more than 35 million client requests, and learned upwards of 400,000 different ways in which questions can be asked.

Voice assistants are capable of handling customer conversations at the early stages of financial planning. Over time, this self-service option will free financial advisors to focus on the higher-value conversations towards the end of the decision process.

The Digital Banking Future

After disruptions to business due to COVID-19, and many customers concerned about their financial health, global banking and financial organizations must work even harder to differentiate themselves, in order to retain existing, and attract new customers. Personalized digital touchpoints are key drivers to this multi-channel and digital future.

The most progressive global banking and financial organizations are already embracing an effective data analytic and technology strategy to support decision-making and to set themselves apart from the competition.

The original version of this article can be found at FinTech.

LEARN MORE

Contact us today to learn how Lucidworks can help your team create powerful search and discovery applications for your customers and employees.